Do you really understand the landscape of retirement communities in 2023? They're not just for the old

The growing scale of the retirement communities industry is impressive, accounting for more than 300,000 dwellings. And there's two very different types of community to choose from.

On the weekend just gone some dear extended family members made a big announcement. “We’ve sold our apartment at the Gold Coast and we’re moving five and a half hours north to a retirement community.” Their faces were alight at the idea.

This couple are in their early 70s and pretty healthy and health-conscious. They moved to the sleepy seaside town in the Gold Coast early in their retirement, and lived in a lovely apartment with friends all around them. But times are a changing, and their sleepy town is turning into a developers’ mecca. So it is time for a change. Armed with a list of criteria, they set off to find a new lifestyle community with an available house near them and the only one they could find that met their long list (beach, newness, size, sleepy town, vibe) was 5.5 hours from their home (only 3.5 hours from ours apparently). Their faces light up at the prospect of what they are gaining with this move. And we’re excited for them.

And that my friends is an opener to a deep-dive into retirement communities and how the different players in the industry fit into real, modern retired life. This rather wonderful and increasingly progressive industry is so poorly hidden behind big gates and fences, and simply not understood by the average over-50 today. So let’s change that. Today, whether you’re ready to discuss them or not, I want you to understand the different players in this sector, what they offer and why they offer it so you can see the potential role that a retirement community could play in your life - to your own benefit, as you age. If you feel like it’s an old persons issue - pretend you’re reading this for your parents’ benefit.

Know I’m not being paid for any of this! This is my honest, independent view.

Have you ever lived alone?

To start, I want you to stop and think about the last time you lived alone. I am one of the fortunate people who has actually never done so, at the age of 47. I grew up in my parent’s home, moved to London with my boyfriend, moved home with him, married him and grew a family. Our children still live at home, but the years are nearing when they will fly the nest, and we become ‘empty nesters’ adventuring through the next stage of pre-retired and retired life as much as our health allows before we hit frailty. Inevitably, one of us will die first - (if we don’t divorce on the journey) and the other will live alone for a period of time.

It isn’t healthy to live alone. In fact, the longest study of longevity, the Harvard Study of Adult Development concluded that close relationships with other people, more than money or fame, are what keep people happy throughout their lives. Those ties protect people from life’s discontents, help to delay mental and physical decline, and are better predictors of long and happy lives than social class, achievements or even genetics.

Retirement communities, an industry transformed

Last week I dropped into the National Retirement Living Summit on the Gold Coast for the largest retirement industry event of its kind in history. The growing scale and importance of the retirement communities industry as the Boomer emerges is impressive. According to Tony Randello, the CEO of Aveo Group and the President of the Retirement Living Council, the retirement communities industry is now the single largest format of alternative accommodation in the country accounting for 300,000 homes, 230,000 of which are in retirement villages and 70,000 are in lifestyle communities. Six years ago this sector was in turmoil after a Four corners story that exposed issues with contracts. And they’re humble and upfront as a sector about how much legislative work has been done, and will continue to be done to offer consumers transparency so this doesn’t happen again. There was no sign of turmoil. Covid shone a fabulous light on the benefits of living in a community as you age. And new developments are really selling it for us all.

Two tiers of retirement community living

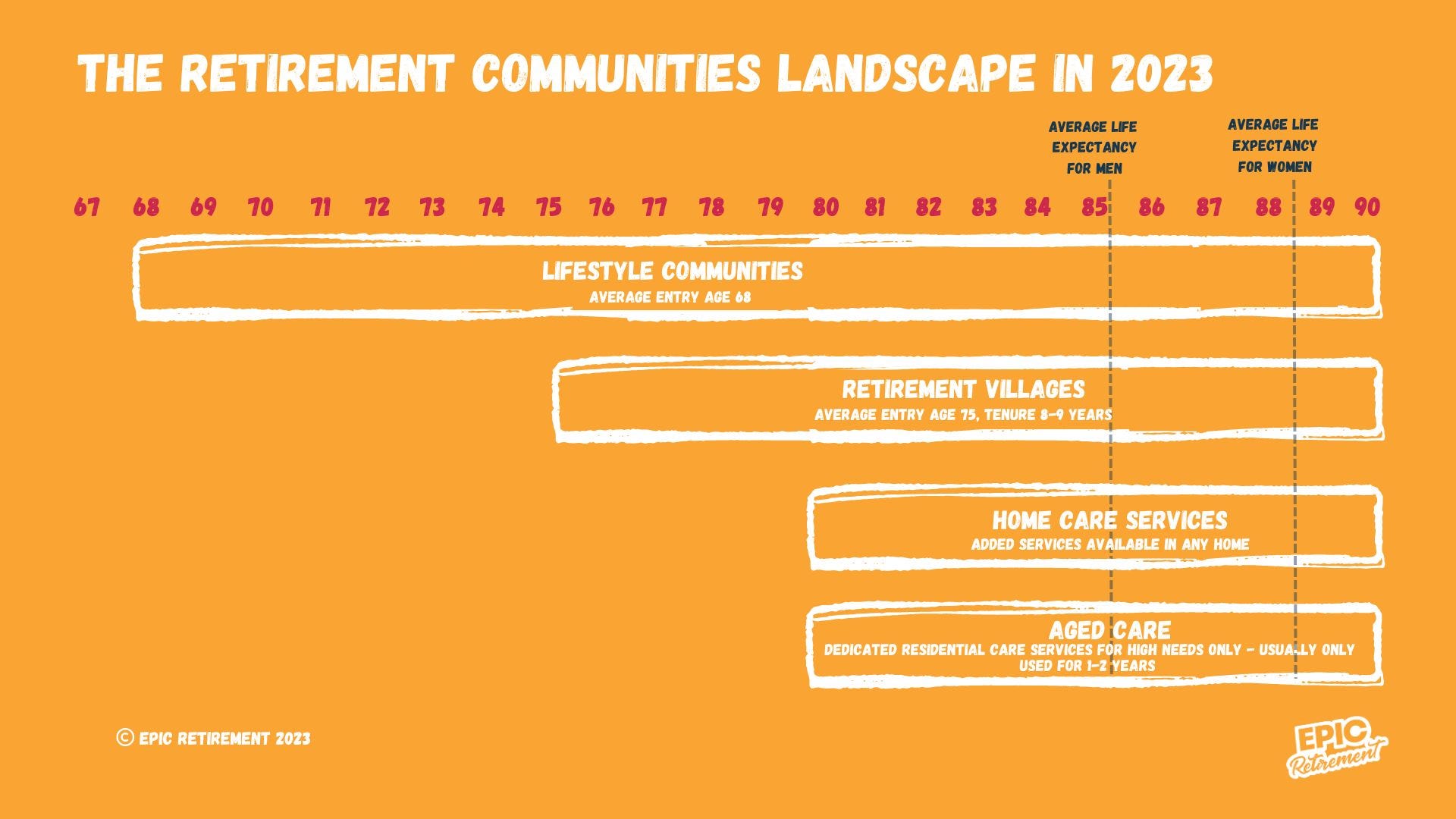

In Australia there are two very different tiers of retirement communities. They look the same to the unaware eye, but each is bought, sold and consumed by people with very different needs, at different stages of life. And they are each legislated by completely different parts of government. It boggles me that nobody explains this simply to the buying market. They also fail to explain that home care and aged care are nothing like retirement communities - although need to be understood in the second half of life too. Retirement communities are for independent living, care services are designed to serve you when you are no longer independent. So please don’t discuss them in the same sentence. Home care is a service that will come to ANY home (including a retirement village), and aged care is simply hard-core residential care. No resemblance to retirement living at all I’m afraid. Retirement villages don’t provide home care services.

All four parts of the retirement housing and care industry play an important role in retirement. One that every retiree should understand better and see in perspective. It can be hard to do so because each tier of the industry speaks of itself in isolation but there’s huge overlaps. It seems crazy that one organisation doesn’t bring it all together. Maybe one day they will.

So let’s put them in context of how they fit into an average person’s life and talk about the real people who live in each and what they pay for.

Lifestyle Communities - a place to live well

The land lease, lifestyle or over-55s community is a serviced property offering. It is a type of community with low set housing, built to standardised designs for efficiency, usually positioned within a gated land development. Newer communities are jam-packed with facilities like pools, gyms, bowling greens, outdoor dining areas, community centre, theatres, caravan parking, men's sheds, gardens and more. You buy a standalone house, technically relocatable, and lease the land from the developers paying a fortnightly rental fee. If you are eligible for the pension you’ll likely be able to qualify for rent assistance on the land rental fee. There’s no stamp duty as you don’t own the land, no exit fees and most developers allow residents to share in the capital gain. The average age of people living in a land lease community in Australia is currently 68 years, and the average price of the housing is not benchmarked nationally but is usually ~75% of the typical downsizer’s current home value according to Corelogic Stockland Research.

Land Lease rental fees usually start at around $200 per week, conveniently maximising a resident’s use of rent assistance which supports approximately 30% of the fees if they can get it.

Land Lease communities have come a long way in 10 or 15 years. The housing standards offered by these developers now rival some of the best offerings from house-and-land developers. And the community facilities are really enviable. They used to be frowned on as modular housing and offered on old caravan park sites with a cheap community centre adjacent to van parks, and some older ones still are. While others are becoming modern, facility-packed community developments with beautifully designed smaller homes presented on some of the most attractive seaside and urban land holdings. Sure, some of these sites were once held as caravan sites but many have been purchased specifically for the land lease development. They’re certainly worth a second look, especially the newer developments. The wait lists for stock in this industry will blow your mind. You can find yourself waiting up to 2 years for a project to be built in an area you are looking for with high demand right now.

Land lease communities are developed under different legislation in every state. In New South Wales they operate under the Residential (Land Lease) Communities Act 2013, while in Victoria they operate under the Residential Tenancies Act 1997 (Part 12A - Long-stay park agreements) and in Queensland, they operate under the Manufactured Homes (Residential Parks) Act 2003. This in itself might not seem significant, but the reality is that the obligations, terminology, contracts and dispute resolution differs in each state. So make sure you understand it if you’re looking.

Retirement Villages - a place to age well - with safety and support

Retirement villages are a pretty impressive place to grow older. And in reality, you shouldn’t assume they are a pure real estate purchase. They are, in my opinion, a type of ‘housing and community as a service’ business, providing housing, community, security and some health and wellbeing services all in one premise. They look like property developments, but the reality is, they are much more than that, and should be seen as the place most effectively designed for you to ‘age in place’. They are paid for under a range of contract options, the most common of which is the deferred management fee (DMF), where you pay a lower upfront price than the market would charge for an apartment of a similar standard, and top this up with a deferred management fee paid when you leave (or die). This can allow you to access much higher quality housing than you could afford in the housing market, or allow you to stretch your dollar much further. You will also have to pay a monthly service fee, transparently laid out. And, depending on the contract you select to enter under, you may or may not be able to access rent assistance. The average entry age to a retirement village is now 75 years of age, and the average age of residents is 81 years. People live on average 8-9 years in a community and most reach their median DMF payment of 30% over 5 years.

The ‘average’ price of an independent living unit (ILU) in a retirement village in the latest census was $484,000 to $516,000 and grew by 6.6% over 18 months to December 2022, while national house prices over the same period rose by 26.2%. This equates to 52 percent of the median house price in Australia. And this discount comes from the benefit of the DMF model.

The retirement villages sector is legislated under the Retirement Village Act in each state. The contracts are regulated fairly heavily now, and the industry is working very hard to provide consumers with transparency. And demand is very strong. What was an industry in turmoil six years ago, is now a sector in extraordinary growth, with long wait times for new developments and high occupancy rates.

The differences between the two types of communities are palpable. Lifestyle communities have younger residents, an affordable ‘modular’ house purchase and land rental business model that attracts rent assistance and residents come in at about 67 years of age with a plan to live there for 15-20+ years, if they live that long. There’s no stamp duty and you can participate in the capital gain on exit. In a retirement community, people come at 75, stay for 8-9 years. They usually purchase on a DMF model to access housing at an average 52% of the median house price in an area, with a median DMF of 30% of their purchase price payable after 5 years. They expect and need both community and services to help them age in place.

Both offer extraordinary benefits of living among a like-minded community, and access to facilities and activities that keep people well engaged in life as they grow older. Why would you ever contemplate growing old alone and lonely in a big drafty old house?

I’m thoroughly impressed that my inlaws have chosen to move to a lifestyle community. I hope they’ll come on the podcast one day to tell you their story.

Read on - there’s a lot more below.

Until next week! Make it epic!

Bec Wilson Xx

This week - 1 July financial changes are coming for retirees

The week ahead is an important week in money matters for retirees. There’s two big items to have your eye on.

1. Superannuation mandatory drawdown levels

Outflows from super funds will revert back to mandatory pension levels with the end of the pandemic measures that allowed retirees to draw half that for the last two years. This should see between 30-40% of retirees increasing their drawdowns. The drawdown rate defaults back to the following levels:

Under 65 - 4%

65-74 - 5%

75-79 - 6%

80-84 - 7%

85-89 - 9%

90-94 - 11%

95 or older - 14%

These percentages represent the minimum amount that retirees in the pension phase are required to withdraw from their superannuation funds each year once they reach the specified age range.

2. Pension eligibility changes kick in on 1 July

The Australian government announced a couple of weeks ago they will increase age pension thresholds and income free areas on 1 July 2023 to allow for inflation, effectively increasing eligibility for the pension across the country. The pension amounts don’t change directly, but the amounts you receive in your account if you’re a part pensioner will, as will the number of people who can get a full pension. This is because of an increase to the asset and income floors which define a full pension, and the caps at which you lose access to the pension. They’ve also adjusted the bands for deeming, one of the key measures of the income test. Read all about it here.

Carolyn wrote to me this week to share her own terrific story of moving to a retirement community. It felt like the perfect story to share on this newsletter.

“When my mum passed away I decided it was time for me to downsize. Being a Baby Boomer, I didn’t have a huge superannuation fund to rely on so chose a 3 bedroom, semi-ensuite bathroom home in an over-55s village within my budget.

The village itself is within walking distance to public transport, regional shopping centres, a public hospital and most importantly the local beach where I have belonged to the surf lifesaving club for over 30 years.

There are 169 privately owned lots in the complex and the council has the assistance of a strata management company, which helps us with any tangly issues that arise!

We have regular social functions, an indoor/outside swimming pool heated to 28 degrees year-round and a fully equipped gymnasium. Bingo, cards and quiz nights are regularly advertised and our lawn bowls club regularly meets with other similar villages for inter club activities. Nobody could ask for more in their retirement days.

Making new friends was easy as the social events here are regular and well attended. There are lots of people from all walks of life who join in and contribute in lots of very positive ways. Life is what you put into it, of course and I have always been willing to give it a go and let everyone else do the same if they want to.”

Thanks Carolyn for sharing your story. Please, reach out if you have a great story to share with our community! Send me your stories, podcast inputs or suggest topics and give me feedback on bec@epicretirement.com.au. I’m hungry for epic retirement stories to feature.

Retirement Diaries Podcast: 'Don't learn the hard way' from Financial Counsellor and part-time retiree, Christine Jones

We can learn so many lessons about preparing for retirement simply by talking about the most common problems retirees come to see financial counsellors for. Listen here. Or watch the video on YouTube here (and be sure to subscribe to our Youtube account).

On social media this week

This week in our Epic Retirement Facebook Group, a beautiful poem by Donna Ashworth is going viral among the community. “Don’t prioritise your looks my friend, as they won’t last the journey. Your sense of humor though, will only get better with age. Your intuition will grow and expand like a majestic cloak of wisdom…” Read the whole poem here.

And on our Instagram I talk about how you can boost your longevity by eating and fasting in the second half of life!

Be inspired to send the Epic Retirement Newsletter to your friends

I’ve kicked off a rewards program. If you share this newsletter with your friends and three of them sign up - you will receive this 40 PAGE eguide on concessions in your inbox, valued at $24.95.

IMPORTANT DISCLAIMER: The information provided in this newsletter and all materials by Epically is intended to be general advice and for educational purposes only. It is not personalised financial, investment, or legal advice. The content presented is based on our understanding of current laws and regulations, which may change over time. We recommend consulting with a qualified financial advisor, accountant, or legal professional before making any financial or retirement-related decisions. We make no representations or warranties of any kind, express or implied, regarding the accuracy, completeness, reliability, or suitability of the information shared. Listeners are solely responsible for their own actions and decisions based on the information provided in this podcast.